The 2026 PACE Loan Overhaul: How New CFPB Rules Protect Homeowners Financing Solar and Energy Upgrades

A new Consumer Financial Protection Bureau rule now requires lenders to apply standard mortgage protections to Property Assessed Clean Energy (PACE) loans. The mandate, which took effect in March 2026, forces lenders to verify a borrower's ability to repay before attaching clean-energy debt to their property taxes.

By Factlen Editorial Team

- Consumer Advocates

- Argue that strict underwriting is necessary to protect vulnerable homeowners from predatory door-to-door sales and foreclosure risks.

- Mortgage & Title Industry

- Support the regulations to standardize lending, protect primary mortgage lien priority, and reduce tax-induced mortgage defaults.

- Clean Energy Lenders

- Must adapt their business models to stricter financing requirements, moving away from simple equity-only underwriting.

What's not represented

- · Independent Solar Contractors

- · Local Tax Assessors

Why this matters

PACE loans offer a way to finance solar panels and energy-efficient upgrades without upfront costs, but they can dramatically increase property tax bills and put homes at risk of foreclosure. The new CFPB protections ensure homeowners receive transparent disclosures and are not lured into unaffordable debt, making green upgrades safer to finance.

Key points

- The CFPB's new rule classifies PACE loans as credit, subjecting them to the Truth in Lending Act.

- Lenders can no longer approve PACE loans based solely on home equity; they must verify a borrower's ability to repay.

- Homeowners will now receive standard Loan Estimate and Closing Disclosure forms before signing.

- The rule aims to prevent unexpected property tax spikes that lead to mortgage escrow shortages and foreclosures.

- The mortgage and title industries strongly supported the rule to protect the stability of primary home loans.

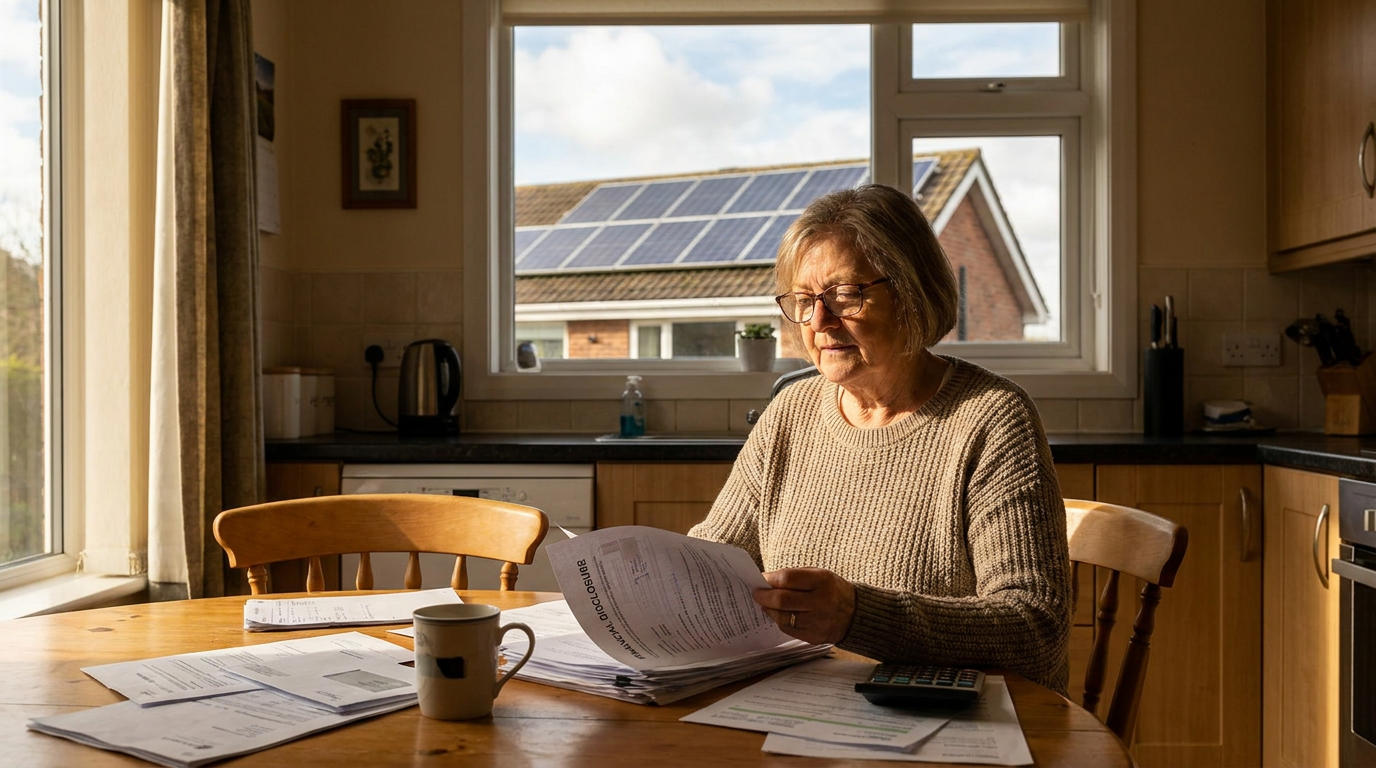

For homeowners looking to install solar panels, upgrade to energy-efficient HVAC systems, or fortify their roofs against disasters, the upfront costs can be daunting. Over the past decade, Property Assessed Clean Energy (PACE) loans emerged as a popular solution, allowing property owners to finance these improvements with zero money down. Instead of a traditional monthly loan payment, the debt is repaid through an annual assessment added to the homeowner's property tax bill.[1][5]

The unique structure of PACE financing made it highly accessible, but it also introduced significant risks. Because the loan is attached to the property itself rather than the individual borrower, the debt transfers to the new owner if the house is sold. More importantly, PACE loans historically operated outside the strict regulatory frameworks that govern traditional mortgages, creating a loophole that left many consumers vulnerable to predatory lending practices.[2][5][6]

Prior to 2026, many PACE lenders approved financing based solely on the amount of equity a borrower had in their home, rather than their actual income or ability to make the payments. This equity-only underwriting model allowed contractors—often utilizing door-to-door sales tactics—to push expensive upgrades with promises that energy savings would offset the costs.[1][2]

The reality for many borrowers was far different. Research conducted by the Consumer Financial Protection Bureau (CFPB) revealed that PACE loans caused property tax bills to surge by an average of $2,700 per year, representing an 88 percent increase for the typical borrower. Furthermore, the interest rates on PACE financing were often around five percentage points higher than those of a standard first mortgage.[1][6]

This sudden spike in property taxes frequently triggered a cascade of financial distress. When a homeowner's tax liability increases, their mortgage servicer must adjust their escrow account to cover the difference, leading to a dramatic jump in their monthly mortgage payment. A $5,000 annual PACE assessment, for example, translates to an unexpected $416 monthly increase in housing costs.[8]

As a result, the CFPB found that PACE borrowers were significantly more likely to fall behind on their primary mortgages compared to homeowners who used other forms of financing. The situation was compounded by the fact that PACE loans typically hold "super lien priority." This means that in the event of a foreclosure, the PACE assessment must be paid off before the primary mortgage lender recovers any funds.[1][4][5][6]

To address these mounting consumer protection and systemic risks, the CFPB finalized a comprehensive rule that fundamentally alters how PACE loans are issued. Mandated by the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018, the new regulations officially took effect on March 1, 2026.[1][3][5]

The cornerstone of the 2026 overhaul is the classification of voluntary PACE assessments as "credit" under the Truth in Lending Act (TILA) and Regulation Z. By bringing PACE financing under the TILA umbrella, the CFPB has effectively closed the regulatory loophole, subjecting these loans to the same stringent oversight as traditional residential mortgages.[2][3][5][7]

The cornerstone of the 2026 overhaul is the classification of voluntary PACE assessments as "credit" under the Truth in Lending Act (TILA) and Regulation Z.

The most immediate impact for homeowners is the implementation of the "ability-to-repay" requirement. Lenders can no longer rely solely on a home's equity to approve a PACE loan. Instead, they are legally required to evaluate a borrower's income, assets, and current debt obligations to ensure they can genuinely afford the increased property tax burden without defaulting on their primary mortgage.[1][2][5][7]

"Today's rule stops unscrupulous companies and salespeople from luring homeowners into unaffordable loans based on false promises of energy savings," CFPB Director Rohit Chopra stated when the rule was finalized. The agency emphasized that homeowners deserve total transparency when putting their financial futures on the line for clean energy upgrades.[1][6]

Transparency is now enforced through standardized documentation. Under the new framework, PACE borrowers must receive the exact same Loan Estimate and Closing Disclosure forms used in traditional real estate transactions. These TILA-RESPA Integrated Disclosure (TRID) forms allow consumers to clearly see the total cost of the loan, the interest rate, and the exact impact on their property taxes before they sign any contracts.[2][4][5]

This standardized disclosure is critical because, as the CFPB noted, most homeowners who took out PACE loans actually qualified for alternative, significantly cheaper forms of financing. By forcing lenders to present the costs in a universally understood format, consumers are now empowered to shop around and compare PACE terms against home equity lines of credit (HELOCs) or personal loans.[1][5]

The regulatory shift has been widely championed by consumer advocacy groups. The Center for Responsible Lending praised the CFPB for curbing practices that disproportionately burdened low-income homeowners and communities of color, noting that the ability-to-repay standards will reinforce equity in the clean energy transition.[2]

The mortgage and banking industries have also been vocal supporters of the 2026 rules. Organizations like the Mortgage Bankers Association (MBA) and the American Land Title Association (ALTA) have long argued that PACE loans upend traditional lien priority and expose primary lenders to increased losses. By requiring strict underwriting, the new rules protect the stability of the broader mortgage market by reducing the likelihood of tax-induced defaults.[3][4][6][7]

While the federal rules establish a strong baseline of protection, the landscape of PACE financing remains highly localized. Currently, while 40 states allow commercial PACE programs, residential PACE loans are primarily active in just three states: California, Florida, and Missouri.[5]

Some states have taken their own legislative action to mitigate the risks associated with PACE financing. Ohio and Minnesota, for example, enacted laws that legally subordinate residential PACE liens to traditional mortgages, ensuring that the primary mortgage lender retains priority in the event of a foreclosure.[3][6]

For homeowners considering solar panels or energy-efficiency upgrades in 2026, the financing landscape is now significantly safer. The days of signing a tablet on the doorstep and unknowingly jeopardizing a home's mortgage are effectively over.[1][2]

By forcing the clean energy financing sector to adopt standard banking practices, the CFPB's rule ensures that the transition to sustainable housing does not come at the expense of consumer financial security. Homeowners can now invest in their properties with the confidence that their financing is transparent, affordable, and legally protected.[1][2][5][7]

How we got here

2018

Congress passes the Economic Growth, Regulatory Relief, and Consumer Protection Act, mandating the CFPB to regulate PACE loans.

May 2023

The CFPB releases its proposed rules to apply Truth in Lending Act (TILA) protections to PACE financing.

December 2024

The CFPB officially finalizes the rule, classifying PACE assessments as consumer credit.

March 2026

The CFPB's final rule officially takes effect, requiring lenders to verify a borrower's ability to repay.

Viewpoints in depth

Consumer Protection Advocates

Focusing on the financial safety of vulnerable homeowners.

Consumer watchdogs and the CFPB have long warned that PACE loans were being aggressively marketed to low-income homeowners and communities of color. Because the loans were previously approved based solely on home equity, advocates argue that unscrupulous contractors used door-to-door sales tactics to push unaffordable upgrades. By enforcing the 'ability-to-repay' standard, these groups believe the new rules will stop predatory lending and prevent a wave of tax-induced foreclosures.

The Mortgage Industry

Prioritizing the stability of primary home loans and lien priority.

Traditional mortgage lenders and title companies view PACE loans as a systemic risk because they hold 'super lien priority'—meaning the PACE debt gets paid before the primary mortgage in a foreclosure. The industry strongly supported the CFPB's intervention, arguing that unexpected $2,700 property tax hikes were causing massive escrow shortages and forcing otherwise stable borrowers into mortgage delinquency. For banks, the new rules bring much-needed standardization to an unregulated corner of the housing market.

Clean Energy Contractors

Navigating a slower, more rigorous sales environment.

For the contractors who install solar panels, impact windows, and efficient HVAC systems, the 2026 rules represent a significant operational shift. The days of closing a sale on the doorstep with a quick equity check are over. Installers and specialized PACE lenders must now wait for full income and debt verification, which extends the sales cycle. While the rules make the financing safer, some in the industry worry the added friction could slow the adoption of residential green energy upgrades.

What we don't know

- Whether the stricter financing requirements will significantly slow down residential solar adoption in states like California and Florida.

- How quickly specialized PACE lenders will adapt their software and sales processes to comply with the new TILA disclosure requirements.

Key terms

- PACE Loan

- Property Assessed Clean Energy financing, a system that allows homeowners to pay for energy upgrades through their annual property tax bills.

- Truth in Lending Act (TILA)

- A federal law designed to protect consumers against deceptive lending practices by requiring clear disclosure of loan terms and costs.

- Ability-to-Repay (ATR)

- A regulatory standard requiring lenders to verify a borrower's income, assets, and debt obligations before approving a loan.

- Escrow Shortage

- A deficit in a homeowner's mortgage escrow account, often caused by a sudden increase in property taxes, resulting in higher monthly mortgage payments.

- Super Lien Priority

- A legal status where a specific debt, such as a property tax assessment, must be paid off before the primary mortgage in the event of a foreclosure.

Frequently asked

Do I still have to pay upfront for solar panels with a PACE loan?

No. PACE loans still allow homeowners to finance energy upgrades with zero upfront costs, but lenders must now verify you can afford the long-term payments.

Will a PACE loan affect my monthly mortgage payment?

Yes. Because PACE loans are repaid through property taxes, your mortgage servicer will likely increase your monthly escrow payment to cover the higher tax bill.

Are PACE loans available in every state?

While many states have commercial PACE programs, residential PACE loans are currently only active in a few states, primarily California, Florida, and Missouri.

Can I lose my home if I fall behind on a PACE loan?

Yes. Because PACE loans are attached to your property taxes, failing to pay the assessment can lead to a tax lien and eventual foreclosure.

Sources

Source coverage

8 outlets

3 viewpoints surfaced

[1]Consumer Financial Protection BureauConsumer Advocates

CFPB Finalizes Rule to Protect Homeowners from Predatory Clean Energy Loans

Read on Consumer Financial Protection Bureau →[2]Center for Responsible LendingConsumer Advocates

CFPB Finalizes Rule to Protect Homeowners from Predatory PACE Loans

Read on Center for Responsible Lending →[3]Mortgage Bankers AssociationMortgage & Title Industry

MBA Statement on CFPB Final Rule on PACE Loans

Read on Mortgage Bankers Association →[4]American Land Title AssociationMortgage & Title Industry

CFPB Issues Final Rule on PACE Loans

Read on American Land Title Association →[5]JD SupraClean Energy Lenders

CFPB Finalizes Rule Applying Standard Mortgage Protections to Residential PACE Loans

Read on JD Supra →[6]National Mortgage ProfessionalMortgage & Title Industry

CFPB Finalizes Rule On PACE Loans

Read on National Mortgage Professional →[7]American Bankers AssociationMortgage & Title Industry

CFPB finalizes rule to apply TILA requirements to residential clean energy loans

Read on American Bankers Association →[8]Dunivan Law GroupClean Energy Lenders

What Did the BRIDGE v. CFPB Ruling Decide?

Read on Dunivan Law Group →

Every angle. Every day.

Get shopping stories with full source coverage and perspective breakdowns delivered to your inbox.