The AI Boom's Hidden Bargain: Why Memory Chip Stocks Are Defying Tech Valuation Trends

While logic chipmakers command astronomical market premiums, the companies producing the high-bandwidth memory essential for AI remain surprisingly cheap. A fundamental shift in how memory is manufactured and sold is challenging Wall Street's traditional boom-and-bust assumptions.

By Factlen Editorial Team

- Structural Bulls

- Argue that long-term contracts and custom HBM architecture have permanently ended the memory boom-and-bust cycle.

- Cycle Skeptics

- Believe that the massive build-out of new factories will inevitably lead to oversupply once AI infrastructure spending cools.

- Value Investors

- Focus on the immediate cash flow generation and low forward multiples, viewing memory stocks as a rare bargain in tech.

What's not represented

- · Foundry Operators

- · Retail Tech Consumers

Why this matters

Understanding the valuation gap in semiconductor stocks allows investors to identify potential market inefficiencies in the AI sector. As memory transitions from a cyclical commodity to a contracted necessity, it could represent one of the few remaining value plays in a highly priced tech market.

Key points

- Memory chip manufacturers are reporting record revenues due to the massive data requirements of generative AI.

- Despite this growth, memory stocks trade at steep discounts compared to the companies designing logic chips.

- The transition to vertically stacked High Bandwidth Memory (HBM) requires long-term contracts, potentially ending the industry's historic boom-and-bust cycles.

- Skeptics warn that the massive ongoing investments in new factory capacity could still lead to an eventual supply glut.

The artificial intelligence revolution has minted unprecedented wealth across the semiconductor sector, pushing the valuations of logic chip designers and equipment manufacturers into the stratosphere. Yet, a peculiar divergence has emerged in the summer of 2026. While the companies designing the computational "brains" of AI systems are priced for perfection, the companies manufacturing the "memory"—the essential components that store the vast datasets these models require to function—are reporting record-breaking revenues but trading at steep discounts. This disconnect highlights a fundamental debate on Wall Street about whether the AI boom has permanently altered the underlying economics of hardware manufacturing.[1]

To understand this valuation gap, one must first examine the changing architecture of modern computing and the historical baggage that memory manufacturers carry. For decades, memory was treated as a standardized, highly commoditized product. Traditional Dynamic Random Access Memory (DRAM) chips were largely interchangeable across the industry. Whether a computer manufacturer bought DRAM from a South Korean giant, an American fabricator, or a Japanese supplier, the end product performed identically. This interchangeability created a notoriously brutal boom-and-bust cycle that trained investors to be deeply skeptical of peak earnings.[5][6]

When demand for personal computers or smartphones rose, memory makers would aggressively expand their factory capacity to capture market share. Because it takes years and billions of dollars to build a new fabrication plant, these capacity expansions often came online simultaneously across the industry. The inevitable result was massive oversupply, crashing component prices, and severe financial write-downs. Wall Street learned to apply a strict "cyclical discount" to these companies, refusing to pay high multiples for earnings that historically evaporated within eighteen to twenty-four months.[2][6]

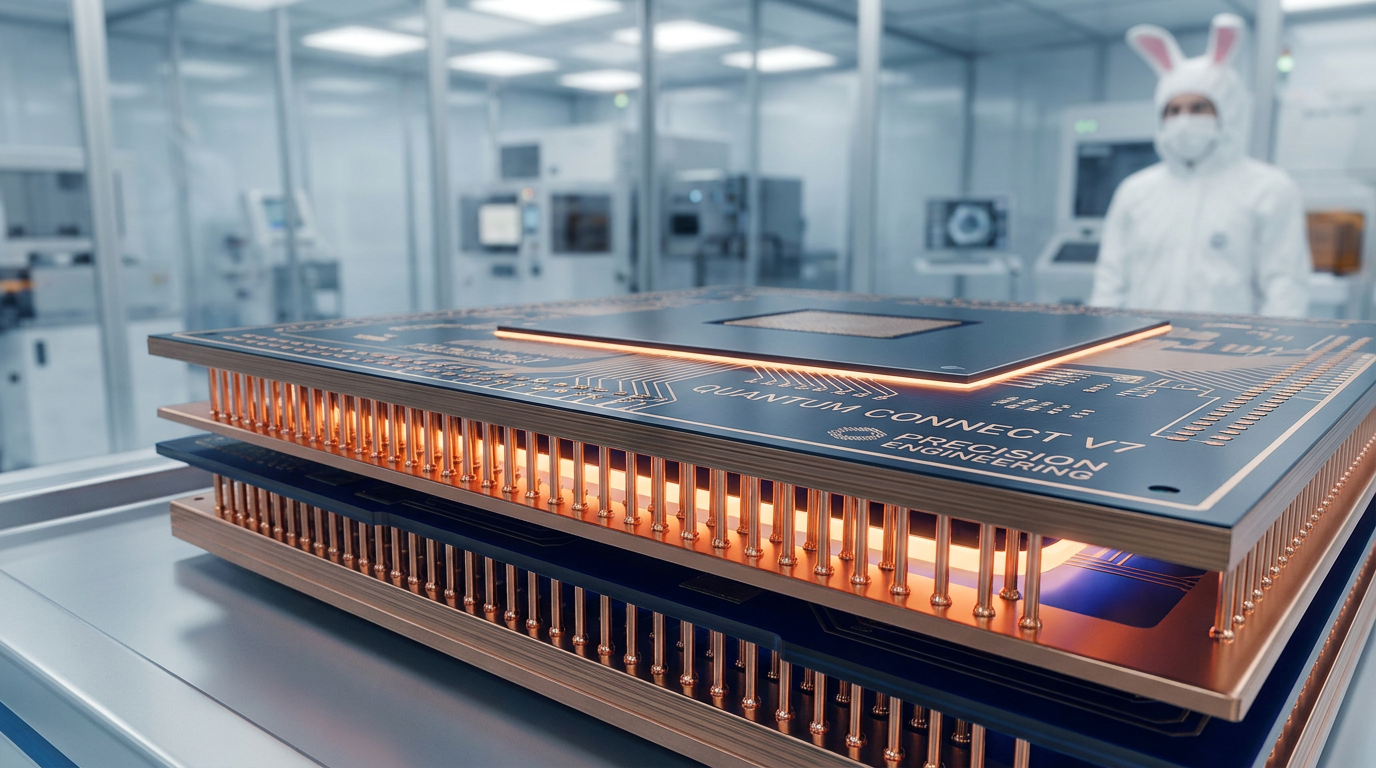

But the advent of generative artificial intelligence has fundamentally altered the physics, engineering, and economics of memory production. Large language models require massive amounts of data to be fed into processing units at blistering speeds. Traditional DRAM, placed flat on a motherboard inches away from the processor, simply cannot move data fast enough—a bottleneck known in computer science as the "memory wall." To break through this wall, the industry had to completely rethink how memory chips are designed, packaged, and integrated into the broader computing system.[3]

The engineering solution to this bottleneck is High Bandwidth Memory (HBM). Instead of placing memory chips side-by-side on a circuit board, engineers thin the silicon wafers to a fraction of a millimeter and stack them vertically. These layers are then connected by microscopic copper pillars called through-silicon vias (TSVs), which allow data to flow directly up and down the stack. This vertical arrangement allows the memory to be placed directly adjacent to the graphics processing unit (GPU) on the same silicon interposer, vastly increasing data transfer rates while simultaneously reducing the power required to move that data.[3][6]

The engineering solution to this bottleneck is High Bandwidth Memory (HBM).

Crucially for the business models of these companies, High Bandwidth Memory is not a plug-and-play commodity. It requires intense, multi-year collaboration between the memory manufacturer, the logic chip designer, and the foundry that packages the final product together. Because of this extreme technical complexity and the tight integration required, memory makers are no longer building chips on speculation and hoping to sell them on the open market. Instead, they are signing long-term, non-cancelable contracts for HBM production years in advance, fundamentally changing their revenue visibility.[4][5]

This shift from building standardized chips for the spot market to building custom stacks on contract theoretically smooths out the dreaded boom-and-bust cycle. Financial filings from the first half of 2026 show the world's top memory manufacturers dedicating up to 40% of their overall capital expenditures specifically to HBM packaging equipment and advanced testing facilities. Because these investments are backed by ironclad purchase orders from the world's largest technology companies, structural bulls argue that memory earnings are now far more durable and predictable than at any point in the industry's history.[4][6]

Despite this profound structural shift in how the industry operates, the broader equity market remains highly skeptical. Forward price-to-earnings ratios for top memory producers currently hover around 12x to 15x. To put that in perspective, logic chip designers and pure-play AI software companies frequently command multiples exceeding 40x, and sometimes much higher. This means that for every dollar of expected profit, investors are willing to pay three times as much for a logic chip company as they are for the memory companies that make those logic chips functional.[1][2]

The cycle skeptics argue that while High Bandwidth Memory is currently severely supply-constrained, the underlying silicon is still subject to the inescapable laws of supply and demand. They point out that every major memory manufacturer is currently racing to expand their HBM capacity as fast as equipment suppliers can deliver the necessary machinery. If the massive, unprecedented build-out of AI data centers by major cloud providers slows down even slightly, the billions invested in new capacity could still result in a glut, albeit a much more technologically advanced and expensive one.[2][6]

Furthermore, the manufacturing yield rates for advanced HBM remain a closely guarded industry secret, adding a layer of opacity that makes conservative investors nervous. Stacking 12 or 16 fragile silicon layers means that a single microscopic defect on any one layer can ruin the entire expensive package. If yield rates do not improve as production scales, the actual profit margins on these cutting-edge chips could be significantly compressed, making the top-line revenue growth look much better than the actual cash flow generated for shareholders.[3][4]

For individual investors and institutional asset managers alike, this presents a classic market inefficiency debate. Either the market is correctly pricing in an inevitable cyclical downturn that will arrive once the initial AI infrastructure build-out is complete, or it is fundamentally mispricing the permanent transformation of memory from a cheap, interchangeable commodity into a bespoke, high-margin necessity. As the AI revolution continues to mature, the resolution of this valuation gap will likely be one of the defining financial stories of the decade.[1][6]

The ripple effects of this memory transformation extend far beyond the chipmakers themselves, creating entirely new sub-industries dedicated to advanced packaging and testing. Companies that manufacture the highly specialized equipment required to bond these delicate silicon layers together are seeing their own order books swell to record levels. This ecosystem-wide mobilization suggests that the shift toward custom, vertically stacked memory is not a temporary trend, but a permanent architectural evolution in how high-performance computers are built. Whether the stock market eventually rewards memory manufacturers with the premium multiples they seek remains to be seen, but their foundational role in the AI economy is now undeniable.[5][6]

How we got here

Late 2022

The launch of advanced generative AI models sparks a massive surge in demand for high-performance computing hardware.

Mid 2023

Severe shortages of High Bandwidth Memory (HBM) emerge as the primary bottleneck for AI data center expansion.

Early 2024

Major memory manufacturers pivot their capital expenditures away from traditional DRAM toward advanced vertical packaging facilities.

June 2026

Memory stocks hit record revenue highs but maintain low valuation multiples as Wall Street debates the longevity of the cycle.

Viewpoints in depth

Structural Bulls

Argue that long-term contracts and custom HBM architecture have permanently ended the memory boom-and-bust cycle.

This camp believes that the fundamental economics of the memory industry have been permanently rewired by artificial intelligence. Because High Bandwidth Memory requires intense, multi-year collaboration between the memory maker, the logic designer, and the packaging foundry, it cannot be built on speculation. Memory manufacturers are now operating on ironclad, non-cancelable contracts that stretch years into the future. Bulls argue that this unprecedented revenue visibility means memory stocks should no longer be penalized with a 'cyclical discount' and deserve valuation multiples closer to their logic-chip peers.

Cycle Skeptics

Believe that the massive build-out of new factories will inevitably lead to oversupply once AI infrastructure spending cools.

Skeptics look at the billions of dollars currently being poured into new fabrication plants and see a familiar, dangerous pattern. While they acknowledge that HBM is currently supply-constrained, they argue that the underlying silicon is still subject to the laws of supply and demand. If the major cloud providers eventually slow their frantic pace of data center construction, the massive new capacity coming online in 2027 and 2028 will have nowhere to go. In this view, the current boom is just a technologically advanced version of the same cycles that have historically crushed memory margins.

Value Investors

Focus on the immediate cash flow generation and low forward multiples, viewing memory stocks as a rare bargain in tech.

For value-oriented asset managers, the debate over the long-term cycle is secondary to the immediate financial reality. With logic chip designers trading at 40x forward earnings or higher, the broader semiconductor sector has become prohibitively expensive for traditional value funds. Memory manufacturers, trading at 12x to 15x forward earnings while generating record cash flows, represent one of the few remaining ways to gain exposure to the AI infrastructure build-out without paying exorbitant premiums. They argue that even if a cyclical downturn eventually arrives, the current stock prices already reflect that pessimism, providing a margin of safety.

What we don't know

- Whether the manufacturing yield rates for 12-layer and 16-layer HBM stacks will improve enough to maintain high profit margins.

- How long the major cloud providers will sustain their current, unprecedented pace of AI data center capital expenditures.

- If Wall Street will ever permanently remove the 'cyclical discount' penalty from memory manufacturer valuations.

Key terms

- Forward P/E Ratio

- A valuation metric that compares a company's current stock price to its expected earnings per share over the next 12 months.

- Logic Chip

- The processors (like CPUs and GPUs) that perform calculations and act as the 'brains' of a computer, distinct from memory chips which store data.

- Through-Silicon Via (TSV)

- Microscopic vertical copper connections that pass completely through a silicon wafer, allowing stacked chips to communicate directly with each other.

- Yield Rate

- The percentage of manufactured chips on a silicon wafer that function correctly and can be sold, a critical metric for profitability.

Frequently asked

What is High Bandwidth Memory (HBM)?

HBM is a type of computer memory where silicon chips are stacked vertically rather than laid flat. This allows data to travel much faster to the processor, which is essential for training artificial intelligence models.

Why are memory stocks historically considered cyclical?

In the past, memory was a standardized commodity. When demand rose, all manufacturers would build new factories at the same time, leading to massive oversupply and crashing prices a few years later.

Why is the valuation gap so large right now?

Investors are willing to pay high premiums for the companies designing AI processors, but they remain fearful that memory manufacturers will eventually overproduce and crash their own prices, leading to a discounted valuation.

Sources

Source coverage

6 outlets

3 viewpoints surfaced

[1]MarketWatchValue Investors

Memory stocks are having their best year ever. Why do they still look so cheap?

Read on MarketWatch →[2]BloombergCycle Skeptics

Memory Chipmakers Ride AI Wave, But Multiples Lag Logic Peers

Read on Bloomberg →[3]arXiv

Architectural Implications of High Bandwidth Memory in Deep Learning Accelerators

Read on arXiv →[4]SECValue Investors

Micron Technology, Inc. Form 10-Q (Spring 2026)

Read on SEC →[5]Semiconductor Industry AssociationStructural Bulls

Spring 2026 Global Semiconductor Sales Report: AI Drives Record Memory Demand

Read on Semiconductor Industry Association →[6]Factlen Editorial TeamStructural Bulls

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.